Whether it's for a coffee talk to get to know each other, a project or press enquiry: here you will find the right contact for all your concerns. Contact us now!

We report on current events and our participation at conferences.

Merkle consultant Katharina Konow joined the Cannes Lions Awards in 2021 and shares her project and award highlights in the blog post.

We were at the conference "Innovations in Banking" and share our latest insights with you.

Meet us across our Central region at Salesforce live events in Prague, Zürich, Düsseldorf and Vienna.

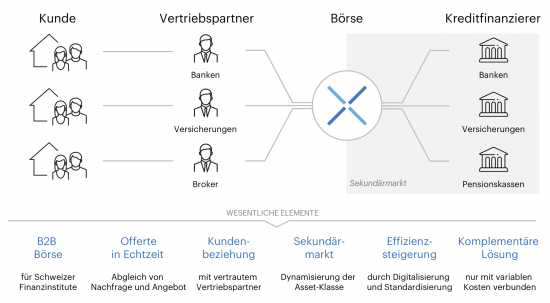

What's new in the banking industry? We report from the conference in Switzerland.

Lecture by Stephanie Chalmers and Mark Seall from Siemens at the Smart Business Day 2019.

Presentation by Christoph Tonini of Tamedia at the Smart Business Day 2019.

Interview with Gilles Despas from Scout24 at the Smart Business Day 2019.

Using this browser can cause mistakes on the website. Using an outdated browser can be dangerous for your computer. We recommend a browser update today.